by

by How To Apply For A Personal Loan Loan applications can often feel overwhelming, but with the right knowledge, you can approach the process confidently. I will guide you through the crucial steps to ensure you understand what lenders are looking for and how to present your financial information effectively. Knowing the potential pitfalls along with the benefits of obtaining a personal loan is crucial. For a detailed breakdown, check out this resource on How to Get a Personal Loan in 7 Steps.

Table of Contents

Understanding Personal Loans

The world of personal loans can seem daunting at first, but understanding the basics will help you navigate it with confidence.

What is a Personal Loan?

While personal loans are unsecured loans that allow you to borrow money for various purposes, such as consolidating debt or financing a large purchase, understanding the terms and conditions is crucial. They come with fixed interest rates and are usually repaid in fixed monthly installments over a set period.

Types of Personal Loans

One of the first steps to applying for a personal loan is understanding the different types available. Here’s a breakdown of the primary categories of personal loans:

| Type | Description |

|---|---|

| Unsecured Loans | Do not require collateral, typically higher interest rates. |

| Secured Loans | Require collateral, often come with lower interest rates. |

| Fixed Rate Loans | Interest rates remain constant throughout the loan term. |

| Variable Rate Loans | Interest rates can fluctuate based on market conditions. |

| Peer-to-Peer Loans | Loans facilitated by online platforms connecting borrowers and lenders. |

Understanding these types allows you to choose wisely based on your financial situation. Each type has its own advantages and disadvantages:

- Unsecured Loans offer flexibility but may come with higher interest rates.

- Secured Loans are beneficial for lower rates but risk forfeiting collateral.

- Fixed Rate Loans provide stability in repayments, aiding in budgeting.

- Variable Rate Loans could lead to unexpected costs if interest rates rise.

- Peer-to-Peer Loans can sometimes offer better rates, but research is necessary.

Knowing what fits your needs best is crucial. The more I understand about personal loans, the better I can make informed choices.

Conclusion

Understanding the fundamentals of personal loans equips you with the necessary knowledge to make smart financial decisions. In this way, you can approach borrowing with a firmer grasp of what each type entails, thus enhancing your confidence in the application process.

Key Factors to Consider

There’s no denying that applying for a personal loan can be a daunting experience. To ensure you approach the process with confidence, it’s crucial to consider the following key factors:

- Credit Score

- Income and Employment Stability

- Debt-to-Income Ratio

After evaluating these elements, you’ll be better prepared to present a compelling application to lenders.

Credit Score

An crucial aspect of your loan application is your credit score. It serves as a reflection of your creditworthiness and influences the interest rates and terms you’ll be offered. Generally, a higher credit score equates to more favorable loan terms.

Income and Employment Stability

For lenders, having stable income and employment history is critical. They want assurance that you can repay the loan without issues, thus a consistent employment record can easily boost your credibility.

With a steady income, you’re showing lenders that you have a reliable flow of money coming in, demonstrating your ability to manage financial obligations. This also often means you need to provide documentation like pay stubs or tax returns to prove your employment status.

Debt-to-Income Ratio

To lenders, your debt-to-income (DTI) ratio is a critical metric indicating how much of your monthly income goes towards debt repayment. A lower DTI suggests you can comfortably handle your current debts and a new loan.

A DTI ratio under 36% is generally considered favorable. However, if your DTI ratio exceeds 43%, you might find it challenging to secure a loan or end up with less favorable terms. It’s crucial to manage your debt responsibly and aim for a balance that allows you to qualify for loans at competitive rates.

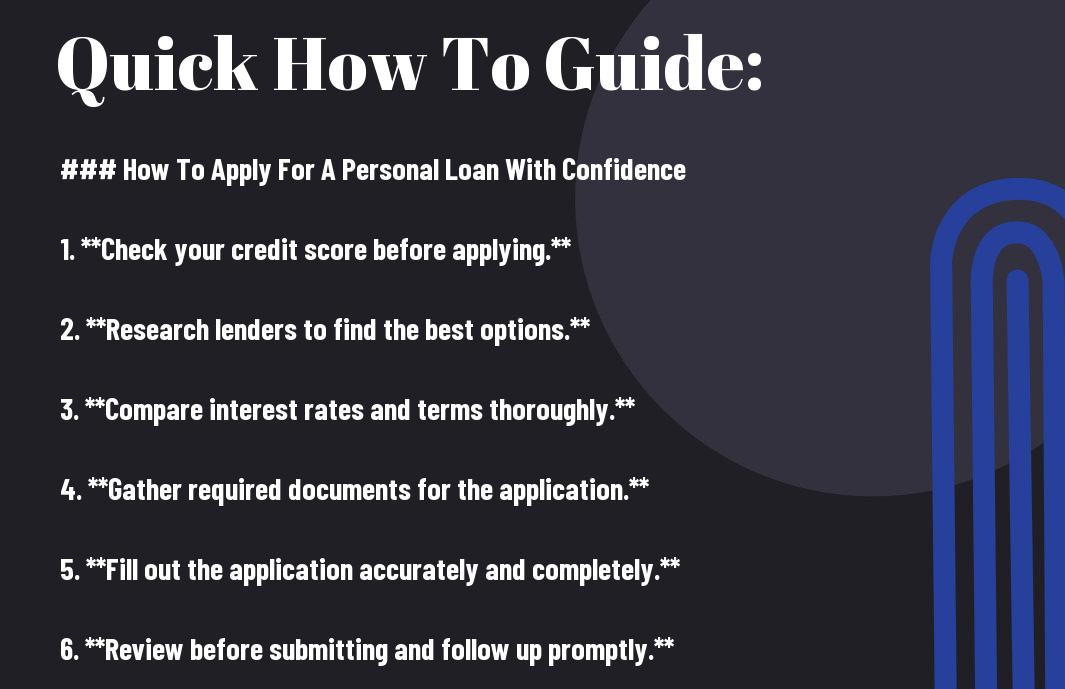

How to Apply for a Personal Loan

Now that we’ve discussed the importance of applying for a personal loan with confidence, let’s explore the steps involved in the application process. Understanding each stage can mitigate any uncertainties and help you prepare effectively.

Researching Lenders

Clearly, the first step in the application journey is to research various lenders. By comparing interest rates, terms, and fees, I can find a loan that best fits my financial situation. It’s crucial to read reviews and gather feedback from previous borrowers to ensure I choose a reputable lender.

Gathering Necessary Documentation

One of the most critical steps is gathering the necessary documentation required for the loan application. These may include proof of income, credit score, employment history, and any other relevant financial information. Ensuring that I have all these documents ready can significantly streamline the process.

Understanding what documents I need, and preparing them in advance, is necessary for a smooth application process. Common items include bank statements, tax returns, and identification proof. Missing even one document can delay approval, so I make sure everything is accurate and readily available.

Completing the Application Process

Any personal loan application process requires attention to detail. I must fill out the application accurately, ensuring all information matches the documentation provided. Mistakes or inconsistencies can raise red flags for the lender and affect my chances of approval.

Plus, many lenders now offer online applications, which can be convenient. However, I still take my time to review each section carefully. Submitting a complete and correct application is vital, as it reflects my seriousness and preparedness to manage the loan responsibly. By double-checking my work, I set myself up for a positive outcome.

Tips for Enhancing Approval Chances

Despite the challenges that may arise when applying for a personal loan, there are several key strategies I can utilize to boost my chances of approval. Here are some imperative tips to consider:

- Maintain a strong credit score

- Avoid taking on new debt before your application

- Build a strong financial profile

- Keep your debt-to-income ratio low

- Provide accurate documentation

Assume that by following these guidelines, I can significantly increase my likelihood of securing the loan I need. How To Apply For A Personal Loan

Improving Your Credit Score

One effective way to enhance my approval chances is by focusing on improving my credit score. A higher score demonstrates my reliability as a borrower, making lenders more inclined to approve my application. To achieve this, I will review my credit report for errors, pay off outstanding debts, and make timely payments on existing loans and credit cards.

Avoiding New Debt Before Application

You should avoid taking on any new debt before applying for a personal loan. New debts can increase my overall financial obligations, affecting my debt-to-income ratio and raising red flags for lenders. It’s imperative to focus on existing financial responsibilities while waiting for my loan application to be processed.

To ensure I am in the best financial position possible, I will resist the temptation to make significant purchases or apply for additional credit cards. By doing this, I will protect my current credit score and maintain a stable financial profile, which is crucial when lenders evaluate my application.

Building a Strong Financial Profile

There’s no doubt that having a solid financial profile is critical to my loan approval chances. This profile includes a careful balance of income, savings, and responsible debt management. By showcasing a consistent income source and demonstrating good financial habits, I can present myself as a trustworthy borrower.

Application of best practices like budgeting effectively, saving for emergencies, and avoiding reckless spending will all contribute to a stronger financial profile. Additionally, I will keep open lines of communication with my lenders and promptly address any concerns they may have regarding my financial history.

Summing up

Hence, as I conclude this guide on how to apply for a personal loan with confidence, I encourage you to take the time to assess your financial needs, research your options thoroughly, and understand the terms of each loan. By doing so, you will empower yourself to make informed decisions that align with your financial goals. Do not forget, being well-prepared not only boosts your confidence but also increases your chances of securing the best loan terms available to you. Make your financial future a priority today!